Recently, AgFunder released their annual report on the state of global Agrifoodtech investment for 2023. The 90 page report is well worth a read in full, but just in case you’re short on time heres our take on their key messages, along with how this fits in with what we’re seeing in the marketplace.

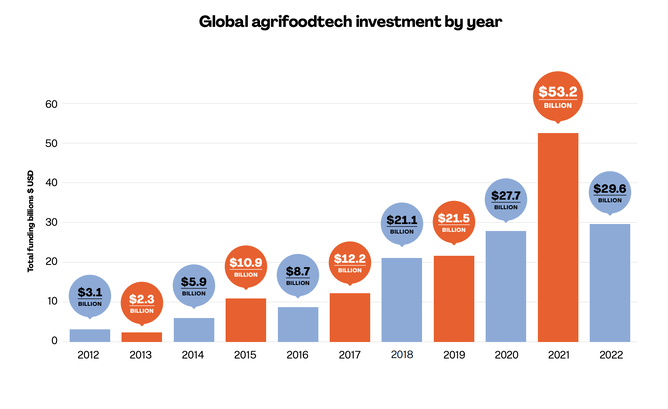

The year-on-year change in investment paints a grim picture of the state of Agrifoodtech investment in 2022, diving 44% to $29.6 billion. Ouch. However, there is more to this story than meets the eye. Looking back to last year’s report, 2021 was entirely different to what we are seeing now, and somewhat of an outlier in the longer-term picture of agrifoodtech investment.

Fuelled by cheap money and overexaggerated tech valuations, 2021 was a standout year in terms of overall investment in this space. The global pandemic in 2020 exposed shortcomings in the food supply chain and dramatic changes in consumer behaviour, triggering increasing investment in technologies addressing this space, and this continued to grow in 2021 as investors gained confidence in signs that the pandemic would be short-lived. This resulted in a record $53.2 billion in investment, an increase of 85% year-on-year.

Placed inside this context, whilst the 2022 investment environment has certainly slowed, the majority of the shift we are seeing from 2021 could be described more as a correction than that of a significant turning point in the industry - as is particularly evident in Figure 1.

Figure 1 - Global agrifoodtech investment by year, AgFunder 2023

While we saw a drop in overall investment in the Agrifoodtech industry, there were also some winners within specific areas.

2022 saw a change in the direction of investment away from downstream technologies, such as eGrocery and restaurant and retail solutions, towards upstream innovations such as ag biotech, farm technology and novel farming systems - particularly those which have some form of focus on…..what for it…..climate change.

This mirrors the trends that Sprout is seeing in the marketplace, evident by the number of companies within the current accelerator cohort that fit within this ‘upstream’ area, and strong growth in the number of companies we see working on climate-relevant solutions - check out CarbonZ and Espy Earth as just two examples.

Reducing food waste was identified in particular as a strong contender for addressing climate change, and highlighted as an area to watch in the future. Sprout Cohort X company CiRCLR works directly in this space assisting businesses to improve the ‘waste to resource’ lifecycle.

The AgFunder report also includes a range of predictions in the Agrifoodtech investment, taken directly from survey responses from venture capital investors focused on the space. Their take on the future is similar to the trends we have seen in the data in 2022, suggesting investment in upstream areas and in particular climate and carbon-related technologies will continue to show strong growth, albeit in the face of a continued correction in the marketplace and in start-up valuations.

Persistent inflation across the board, the current economic climate and outlook, and the continuing situation in Ukraine are seen as significant boulders for Agrifoodtech investment in the future, most of which are unlikely to be resolved within the next 12 months.

Beyond climate solutions, the most significant areas of growth are predicted to be in artificial intelligence (you should check out Sprout Portfolio company Aimer Farming on some clever use of AI) and biotechnology solutions, with some VCs still expecting alternative proteins and vertical farming to make a strong showing despite a slow year in 2022. VCs are expecting to see a shift in thinking from globalisation to more emphasis on locally-sourced food and deflationary technologies and products, across the entire value chain,

Overall, a mixed year for Agrifoodtech investment, and indications show we can likely expect the same over the next 12 months. Investors are showing some clear signs of favouritism towards certain segments, a lot of which are not the same segments we have seen come out as winners historically. It is no doubt a turbulent time for the industry, but also a period of opportunity, particularly for companies willing to listen to what investors are asking of them, ensuring they’re connected and well-prepared to be in the best position to attract investment.